Extrapolate values in Pandas DataFrame

It's very easy to interpolate NaN cells in a Pandas DataFrame:

In [98]: df

Out[98]:

neg neu pos avg

250 0.508475 0.527027 0.641292 0.558931

500 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

[12 rows x 4 columns]

In [99]: df.interpolate(method='nearest', axis=0)

Out[99]:

neg neu pos avg

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

[12 rows x 4 columns]

I would also want it to extrapolate the NaN values that are outside of the interpolation scope, using the given method. How could I best do this?

Answer

Extrapolating Pandas DataFrames

DataFrames maybe be extrapolated, however, there is not a simple method call within pandas and requires another library (e.g. scipy.optimize).

Extrapolating

Extrapolating, in general, requires one to make certain assumptions about the data being extrapolated. One way is by curve fitting some general parameterized equation to the data to find parameter values that best describe the existing data, which is then used to calculate values that extend beyond the range of this data. The difficult and limiting issue with this approach is that some assumption about trend must be made when the parameterized equation is selected. This can be found thru trial and error with different equations to give the desired result or it can sometimes be inferred from the source of the data. The data provided in the question is really not large enough of a dataset to obtain a well fit curve; however, it is good enough for illustration.

The following is an example of extrapolating the DataFrame with a 3rd order polynomial

f(x) = a x3 + b x2 + c x + d (Eq. 1)

This generic function (func()) is curve fit onto each column to obtain unique column specific parameters (i.e. a, b, c, d). Then these parameterized equations are used to extrapolate the data in each column for all the indexes with NaNs.

import pandas as pd

from cStringIO import StringIO

from scipy.optimize import curve_fit

df = pd.read_table(StringIO('''

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 NaN NaN NaN NaN

1000 0.650000 0.571429 0.653983 0.625137

2000 NaN NaN NaN NaN

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN'''), sep='\s+')

# Do the original interpolation

df.interpolate(method='nearest', xis=0, inplace=True)

# Display result

print ('Interpolated data:')

print (df)

print ()

# Function to curve fit to the data

def func(x, a, b, c, d):

return a * (x ** 3) + b * (x ** 2) + c * x + d

# Initial parameter guess, just to kick off the optimization

guess = (0.5, 0.5, 0.5, 0.5)

# Create copy of data to remove NaNs for curve fitting

fit_df = df.dropna()

# Place to store function parameters for each column

col_params = {}

# Curve fit each column

for col in fit_df.columns:

# Get x & y

x = fit_df.index.astype(float).values

y = fit_df[col].values

# Curve fit column and get curve parameters

params = curve_fit(func, x, y, guess)

# Store optimized parameters

col_params[col] = params[0]

# Extrapolate each column

for col in df.columns:

# Get the index values for NaNs in the column

x = df[pd.isnull(df[col])].index.astype(float).values

# Extrapolate those points with the fitted function

df[col][x] = func(x, *col_params[col])

# Display result

print ('Extrapolated data:')

print (df)

print ()

print ('Data was extrapolated with these column functions:')

for col in col_params:

print ('f_{}(x) = {:0.3e} x^3 + {:0.3e} x^2 + {:0.4f} x + {:0.4f}'.format(col, *col_params[col]))

Extrapolating Results

Interpolated data:

neg neu pos avg

0 NaN NaN NaN NaN

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 NaN NaN NaN NaN

6000 NaN NaN NaN NaN

8000 NaN NaN NaN NaN

10000 NaN NaN NaN NaN

20000 NaN NaN NaN NaN

30000 NaN NaN NaN NaN

50000 NaN NaN NaN NaN

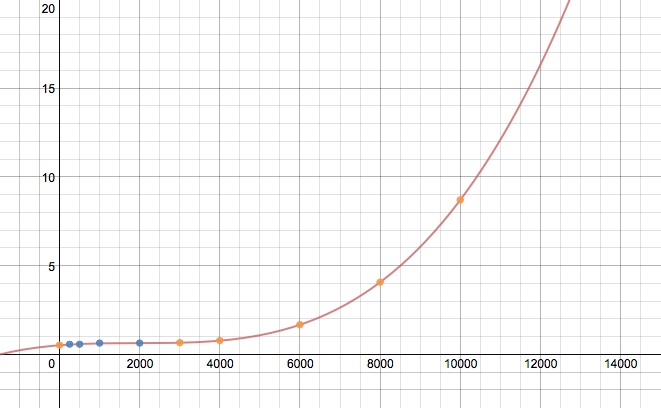

Extrapolated data:

neg neu pos avg

0 0.411206 0.486983 0.631233 0.509807

250 0.508475 0.527027 0.641292 0.558931

500 0.508475 0.527027 0.641292 0.558931

1000 0.650000 0.571429 0.653983 0.625137

2000 0.650000 0.571429 0.653983 0.625137

3000 0.619718 0.663158 0.665468 0.649448

4000 0.621036 0.969232 0.708464 0.766245

6000 1.197762 2.799529 0.991552 1.662954

8000 3.281869 7.191776 1.702860 4.058855

10000 7.767992 15.272849 3.041316 8.694096

20000 97.540944 150.451269 26.103320 91.365599

30000 381.559069 546.881749 94.683310 341.042883

50000 1979.646859 2686.936912 467.861511 1711.489069

Data was extrapolated with these column functions:

f_neg(x) = 1.864e-11 x^3 + -1.471e-07 x^2 + 0.0003 x + 0.4112

f_neu(x) = 2.348e-11 x^3 + -1.023e-07 x^2 + 0.0002 x + 0.4870

f_avg(x) = 1.542e-11 x^3 + -9.016e-08 x^2 + 0.0002 x + 0.5098

f_pos(x) = 4.144e-12 x^3 + -2.107e-08 x^2 + 0.0000 x + 0.6312

Plot for avg column

Without a larger dataset or knowing the source of the data, this result maybe completely wrong, but should exemplify the process to extrapolate a DataFrame. The assumed equation in func() would probably need to be played with to get the correct extrapolation. Also, no attempt to make the code efficient was made.

Update:

If your index is non-numeric, like a DatetimeIndex, see this answer for how to extrapolate them.